7 A Review of Statistics

Acknowledgement: This chapter is largely based on chapter 3 of “Introduction to Econometrics with R”. https://www.econometrics-with-r.org/index.html

The goal of this chapter is

- Review of important concepts in statistics

- Estimation

- Hypothesis testing

- Review of tools from probability theory

- Law of large numbers

- Central limit theorem

7.1 Estimation

- Estimator: A mapping from the sample data drawn from an unknown population to a certain feature in the population

- Example: Consider hourly earnings of college graduates \(Y\) .

- You want to estimate the mean of \(Y\), defined as \(E[Y] = \mu_y\)

- Draw a random sample of \(n\) i.i.d. (identically and independently distributed) observations \({ Y_1, Y_2, \ldots, Y_N }\)

- How to estimate \(E[Y]\) from the data?

- Idea 1: Sample mean \[ \bar{Y} = \frac{1}{n} \sum_{i=1}^n Y_i, \]

- Idea 2: Pick the first observation of the sample.

- Question: How can we say which is better?

7.1.1 Properties of the estimator

Consider the estimator \(\hat{\mu}_N\) for the unknown parameter \(\mu\).

Unbiasdeness: The expectation of the estimator is the same as the true parameter in the population. \[ E[\hat{\mu}_N] = \mu \]

- Consistency: The estimator converges to the true parameter in probability. \[

\forall \epsilon >0, \lim_{N \rightarrow \infty} \ Prob(|\hat{\mu}_{N}-\mu|<\epsilon)=1

\]

- Intuition: As the sample size gets larger, the estimator and the true parameter is close with probability one.

- Note: a bit different from the usual convergence of the sequence.

7.1.2 Sample mean \(\bar{Y}\) is unbiased and consistent

- Showing these two properties using mathmaetics is straightforward:

- Unbiasedness: Take expectation.

- Consistency: Law of large numbers.

Let’s examine these two properties using R.

- Step 1: Prepare a population. Here, I prepare income and age data from PUMS 5% sample of U.S. Census 2000.

- PUMS: Public Use Microdata Sample

- Download the example data here as a .csv file. Put this file in the same folder as your R script file.

# Use "readr" package

library(readr)## Warning: パッケージ 'readr' はバージョン 3.5.3 の R の下で造られましたpums2000 <- read_csv("data_pums_2000.csv") ## Parsed with column specification:

## cols(

## AGE = col_double(),

## INCTOT = col_double()

## )- We treat this dataset as population.

pop <- as.vector(pums2000$INCTOT)- Population mean and standard deviation

pop_mean = mean(pop)

pop_sd = sd(pop)

# Average income in population

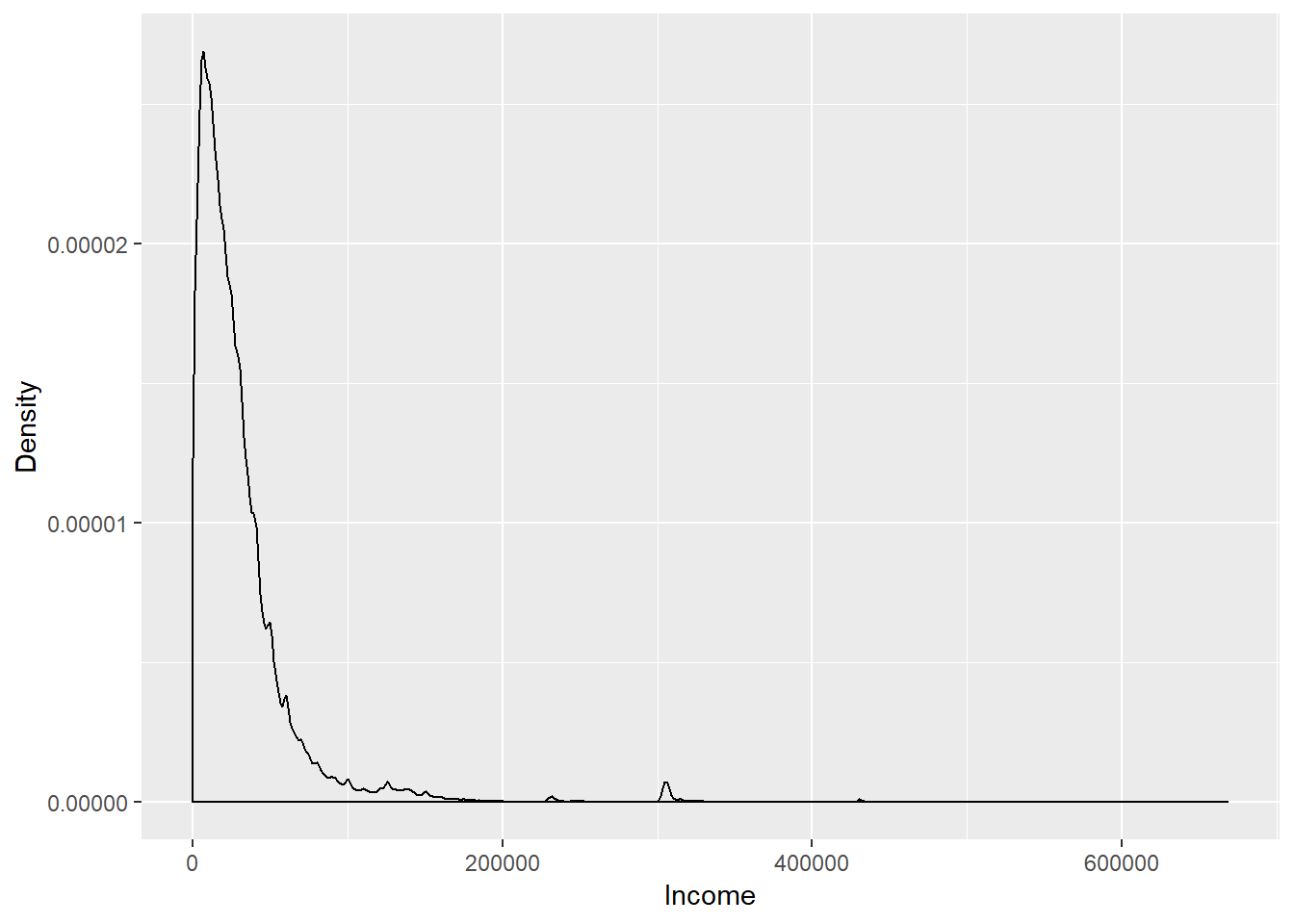

pop_mean## [1] 30165.47# Standard deviation of income in population

pop_sd## [1] 38306.17# income distribution in population

# Note that the unit is in USD.

library("ggplot2")## Warning: パッケージ 'ggplot2' はバージョン 3.5.3 の R の下で造られましたqplot(pop, geom = "density",

xlab = "Income",

ylab = "Density")

- The distribution has a long tail.

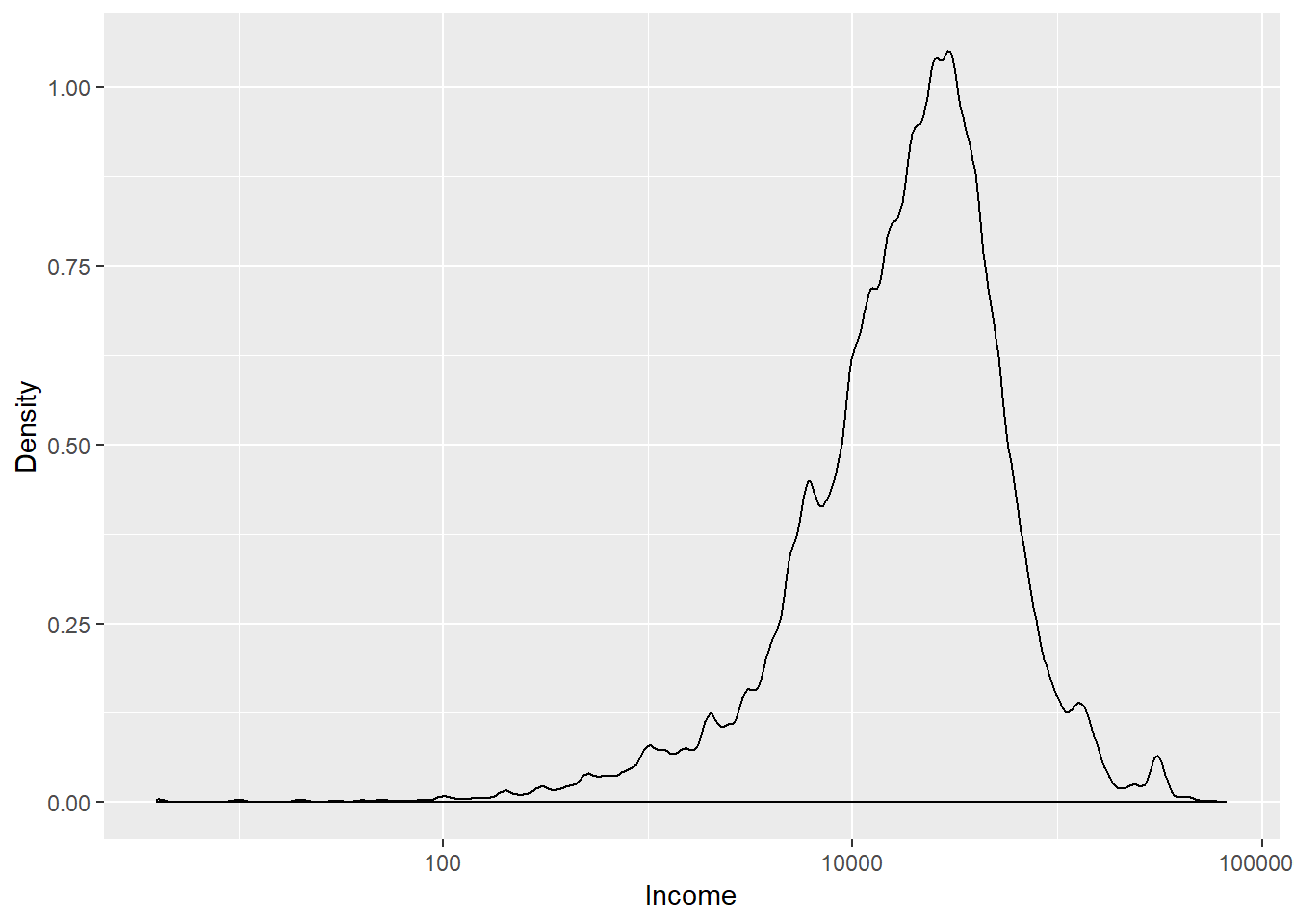

- Let’s plot the distribution in log scale

# `log` option specifies which axis is represented in log scale.

qplot(pop, geom = "density",

xlab = "Income",

ylab = "Density",

log = "x")

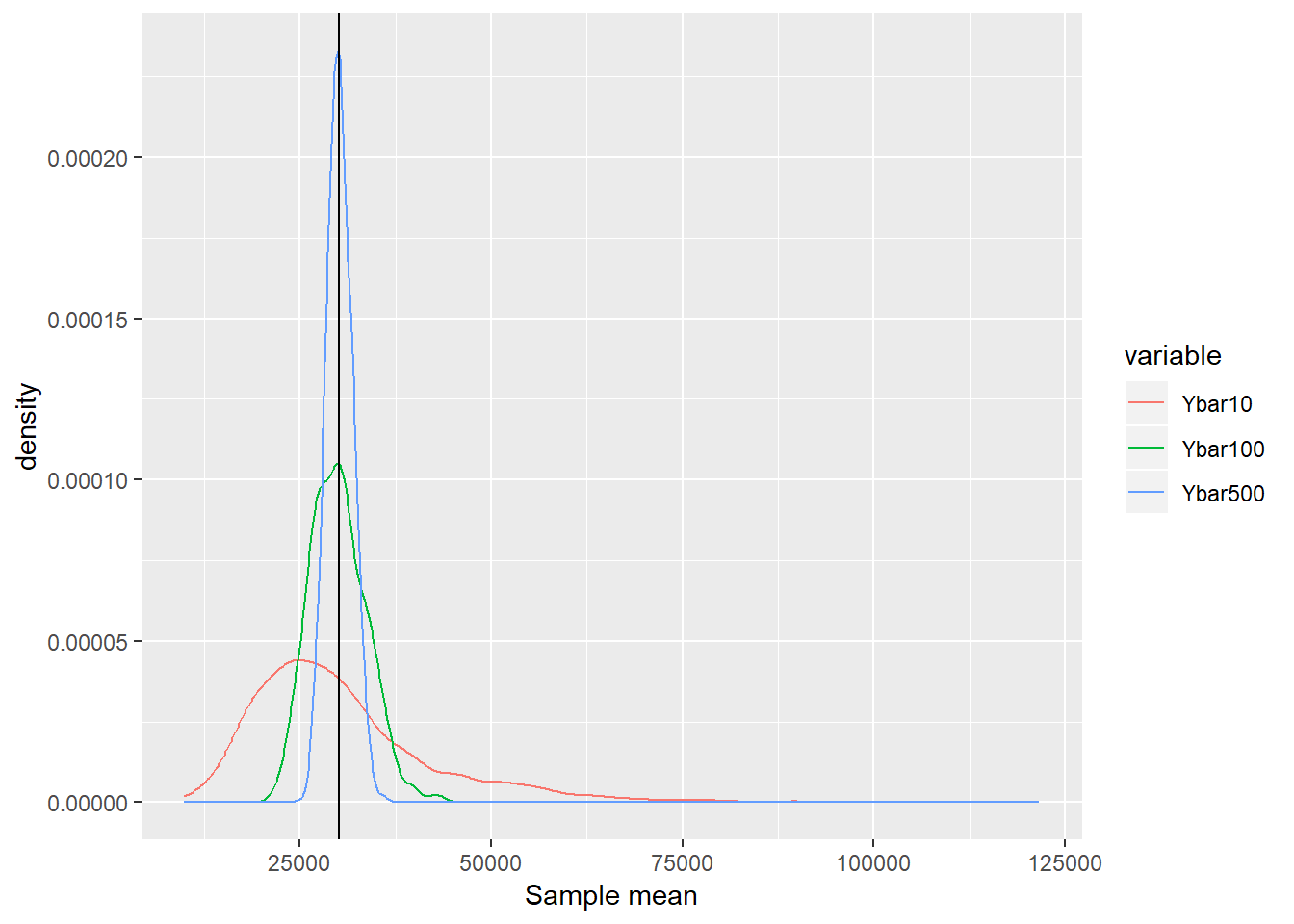

- Let’s investigate how close the sample mean constucted from the random sample is to the true population mean.

- Step 1: Draw random samples from this population and calculate \(\bar{Y}\) for each sample.

- Set the sample size \(N\).

- Step 2: Repeat 2000 times. You now have 2000 sample means.

# Set the seed for the random number. This is needed to maintaine the reproducibility of the results.

set.seed(123)

# draw random sample of 100 observations from the variable pop

test <- sample(x = pop, size = 100)

# Use loop to repeat 2000 times.

Nsamples = 2000

result1 <- numeric(Nsamples)

for (i in 1:Nsamples ){

test <- sample(x = pop, size = 100)

result1[i] <- mean(test)

}

# Simple approach

result1 <- replicate(expr = mean(sample(x = pop, size = 10)), n = Nsamples)

result2 <- replicate(expr = mean(sample(x = pop, size = 100)), n = Nsamples)

result3 <- replicate(expr = mean(sample(x = pop, size = 500)), n = Nsamples)

# Create dataframe

result_data <- data.frame( Ybar10 = result1,

Ybar100 = result2,

Ybar500 = result3)- Step 3: See the distribution of those 2000 sample means.

# Use reshape library

# install.packages("reshape")

library("reshape")## Warning: パッケージ 'reshape' はバージョン 3.5.3 の R の下で造られました# Use "melt" to change the format of result_data

data_for_plot <- melt(data = result_data, variable.name = "Variable" )## Using as id variables# Use "ggplot2" to create the figure.

# The variable `fig` contains the information about the figure

fig <-

ggplot(data = data_for_plot) +

xlab("Sample mean") +

geom_line(aes(x = value, colour = variable ), stat = "density" ) +

geom_vline(xintercept=pop_mean ,colour="black")

# Display the figure

plot(fig)

- Observation 1: Regardless of the sample size, the average of the sample means is close to the population mean. Unbiasdeness

- Observation 2: As the sample size gets larger, the distribution is concentrated around the population mean. Consistency (law of large numbers)

7.2 Hypothesis Testing

7.2.1 Central limit theorem

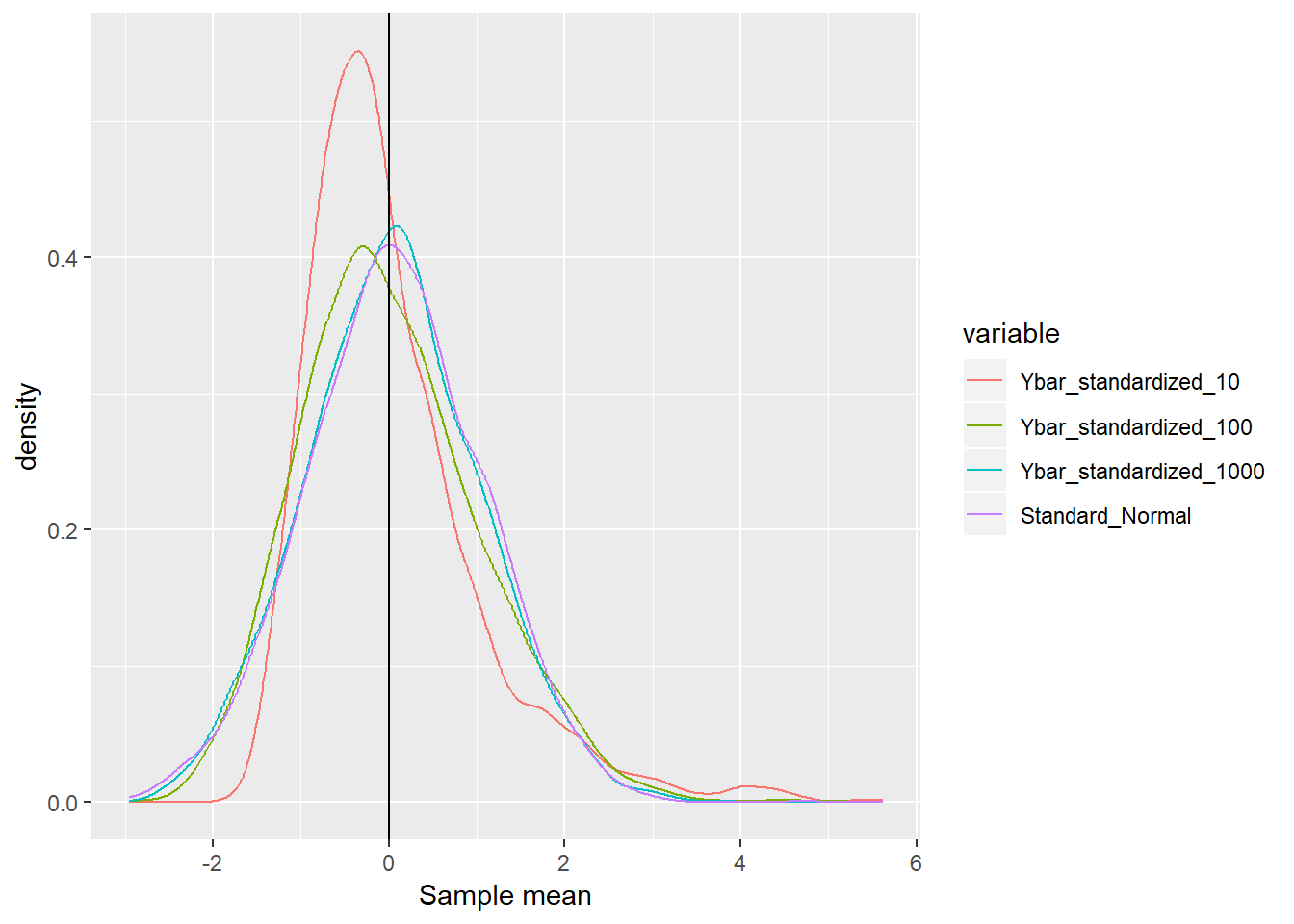

Cental limit theorem: Consider the i.i.d. sample of \(Y_1,\cdots, Y_N\) drawn from the random variable \(Y\) with mean \(\mu\) and variance \(\sigma^2\). The following \(Z\) converges in distribution to the normal distribution. \[ Z = \frac{1}{\sqrt{N}} \sum_{i=1}^N \frac{Y_i - \mu}{\sigma } \overset{d}{\rightarrow}N(0,1) \] In other words, \[ \lim_{N\rightarrow\infty}P\left(Z \leq z\right)=\Phi(z) \]

The central limit theorem implies that if \(N\) is large enough, we can approximate the distribution of \(\bar{Y}\) by the standard normal distribution with mean \(\mu\) and variance \(\sigma^2 / N\) regardless of the underlying distribution of \(Y\).

Let’s examine this property through simulation!!

- Use the same example as before. Remember that the underlying income distribution is clearly NOT normal.

- Population mean \(\mu = 30165.4673315\) and standard deviation \(\sigma = 38306.1712336\). Use these numbers.

# Set the seed for the random number

set.seed(124)

# define function for simulation

f_simu_CLT = function(Nsamples, samplesize, pop, pop_mean, pop_sd ){

output = numeric(Nsamples)

for (i in 1:Nsamples ){

test <- sample(x = pop, size = samplesize)

output[i] <- ( mean(test) - pop_mean ) / (pop_sd / sqrt(samplesize))

}

return(output)

}

# Comment: You can do better without using forloop. Let me know if you come with a good idea.

# Run simulation

Nsamples = 2000

result_CLT1 <- f_simu_CLT(Nsamples, 10, pop, pop_mean, pop_sd )

result_CLT2 <- f_simu_CLT(Nsamples, 100, pop, pop_mean, pop_sd )

result_CLT3 <- f_simu_CLT(Nsamples, 1000, pop, pop_mean, pop_sd )

# Random draw from standard normal distribution as comparison

result_stdnorm = rnorm(Nsamples)

# Create dataframe

result_CLT_data <- data.frame( Ybar_standardized_10 = result_CLT1,

Ybar_standardized_100 = result_CLT2,

Ybar_standardized_1000 = result_CLT3,

Standard_Normal = result_stdnorm)

# Note: If you wanna quicky plot the density, type `plot(density(result1))`. - Now take a look at the distribution.

# Use "melt" to change the format of result_data

data_for_plot <- melt(data = result_CLT_data, variable.name = "Variable" )## Using as id variables# Use "ggplot2" to create the figure.

fig <-

ggplot(data = data_for_plot) +

xlab("Sample mean") +

geom_line(aes(x = value, colour = variable ), stat = "density" ) +

geom_vline(xintercept=0 ,colour="black")

plot(fig)

- As the sample size grows, the distribution of \(Z\) converges to the standard normal distribution.

7.2.2 Hypothesis testing

To be added.