12 Instrumental Variable 1: Framework

12.1 Introduction: Endogeneity Problem and its Solution

- When \(Cov(x_k, \epsilon)=0\) does not hold, we have endogeneity problem

- We call such \(x_k\) an endogenous variable.

- In this chapter, I introduce an instrumental variable estimation method, a solution to this issue.

- The lecture plan

- More on endogeneity issues

- Framework

- Implementation in R

- Examples

12.2 Examples of Endogeneity Problem

- Here, I explain a bit more about endogeneity problems.

- Omitted variable bias

- Measurement error

- Simultaneity

12.2.1 More on Omitted Variable Bias

- Remember the wage regression equation (true model) \[ \begin{aligned} \log W_{i} &=& & \beta_{0}+\beta_{1}S_{i}+\beta_{2}A_{i}+u_{i} \\ E[u_{i}|S_{i},A_{i}] &=& & 0 \end{aligned} \] where \(W_{i}\) is wage, \(S_{i}\) is the years of schooling, and \(A_{i}\) is the ability.

- Suppose that you omit \(A_i\) and run the following regression instead. \[ \log W_{i} = \alpha_{0}+\alpha_{1} S_{i} + v_i \] Notice that \(v_i = \beta_2 A_i + u_i\), so that \(S_i\) and \(v_i\) is likely to be correlated.

- You might want to add more and more additional variables to capture the effect of ability.

- Test scores, GPA, SAT scores, etc…

- However, can you make sure that \(S_i\) is indeed exogenous after adding many control variables?

- Multivariate regression cannot deal with the presence of unobserved heterogeneity that matters both in wage and years of schooling.

12.2.2 Measurement error

- Measurement error in variables

- Reporting error, respondent does not understand the question, etc…

- Consider the regression \[ y_{i}=\beta_{0}+\beta_{1}x_{i}^{*}+\epsilon_{i} \]

- Here, we only observe \(x_{i}\) with error: \[

x_{i}=x_{i}^{*}+e_{i}\] where \(e_{i}\) is measurement error.

- \(e_{i}\) is independent from \(\epsilon_i\) and \(x_i^*\) (called classical measurement error)

- You can think \(e_i\) as a noise added to the data.

- The regression equation is \[ \begin{aligned} y_{i} = & \ \beta_{0}+\beta_{1}(x_{i}-e_{i})+\epsilon_{i} \\ = & \ \beta_{0}+\beta_{1}x_{i}+(\epsilon_{i}-\beta_{1}e_{i}) \end{aligned} \]

- Then we have correlation between \(x_{i}\) and the error \(\epsilon_{i}-\beta_{1}e_{i}\), violating the mean independence assumption

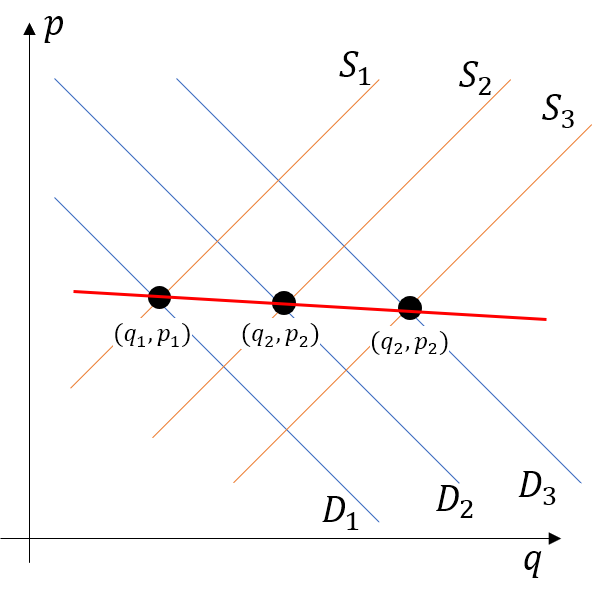

12.2.3 Simultaneity (or reverse causality)

- Dependent variable and explanatory variable (endogenous variable) are determined simultaneously.

- Consider the demand and supply curve \[ \begin{aligned} q^{d} =\beta_{0}^{d}+\beta_{1}^{d}p+\beta_{2}^{d}x+u^{d} \\ q^{s} =\beta_{0}^{s}+\beta_{1}^{s}p+\beta_{2}^{s}z+u^{s} \end{aligned} \]

- The equilibrium price and quantity are determined by \(q^{d}=q^{s}\).

In this case, \[ p=\frac{(\beta_{2}^{s}z-\beta_{2}^{d}z)+(\beta_{0}^{s}-\beta_{0}^{d})+(u^{s}-u^{d})}{\beta_{1}^{d}-\beta_{1}^{s}} \] implying the correlation between the price and the error term.

- Putting this differently, the data points we observed is the intersection of these supply and demand curves.

How can we distinguish demand and supply?

12.3 Idea of IV Regression

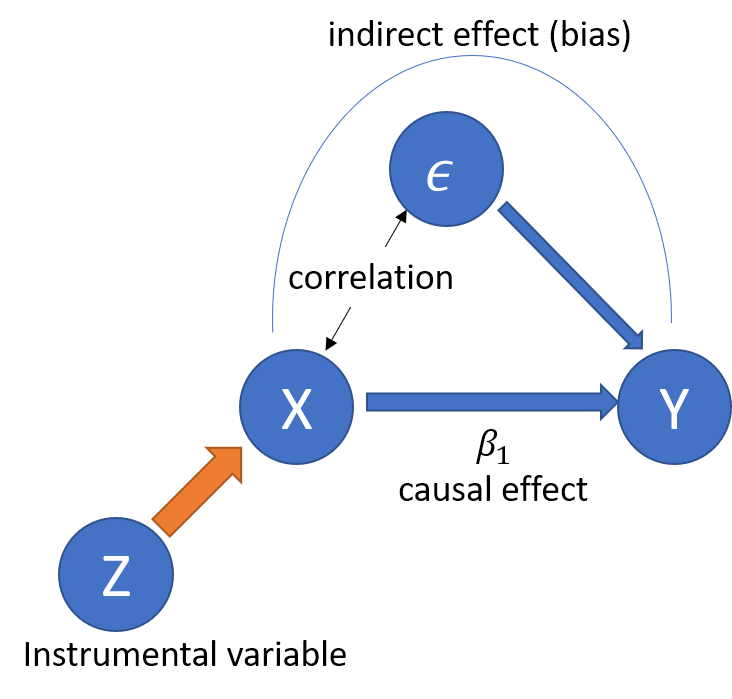

- Let’s start with a simple case. \[ y_i = \beta_0 + \beta_1 x_i + \epsilon_i, \] and \(Cov(x_i, \epsilon_i) \neq 0\).

- Now, we consider another variable \(z_i\), which we call instrumental variable (IV).

- Instrumental variable \(z_i\) should satisfies the following two conditions:

- Independence: \(Cov(z_i, \epsilon_i) = 0\). No correlation between IV and error.

- Relevance: \(Cov(z_i, x_i) \neq 0\). There should be correlation between IV and endogenous variable \(x_i\).

Idea: Use the variation of \(x_i\) induced by instrument \(z_i\) to estimate the direct (causal) effect of \(x_i\) on \(y_i\), that is \(\beta_1\)!.

- More on this:

- Intuitively, the OLS estimator captures the correlation between \(x\) and \(y\).

- If there is no correlation between \(x\) and \(\epsilon\), it captures the causal effect \(\beta_1\).

- If not, the OLS estimator captures both direct and indirect effect, the latter of which is bias.

- Now, let’s capture the variation of \(x\) due to instrument \(z\),

- Such a variation should exist under relevance assumption.

- Such a variation should not be correlated with the error under independence assumption

- By looking at the correlation between such variation and \(y\), you can get the causal effect \(\beta_1\).

Idea IV

12.4 Formal Framework and Estimation

12.4.1 Model

- We now introduce a general framework with multiple endogenous variables and multiple instruments.

- Consider the model \[

\begin{aligned}

Y_i = \beta_0 + \beta_1 X_{1i} + \dots + \beta_K X_{Ki} + \beta_{K+1} W_{1i} + \dots + \beta_{K+R} W_{Ri} + u_i,

\end{aligned}

\] with \(i=1,\dots,n\) is the general instrumental variables regression model where

- \(Y_i\) is the dependent variable

- \(\beta_0,\dots,\beta_{K+R}\) are \(1+K+R\) unknown regression coefficients

- \(X_{1i},\dots,X_{Ki}\) are \(K\) endogenous regressors: \(Cov(X_{ki}, u_i) \neq 0\) for all \(k\).

- \(W_{1i},\dots,W_{Ri}\) are \(R\) exogenous regressors which are uncorrelated with \(u_i\). \(Cov(W_{ri}, u_i) = 0\) for all \(r\).

- \(u_i\) is the error term

- \(Z_{1i},\dots,Z_{Mi}\) are \(M\) instrumental variables

- I will discuss conditions for valid instruments later.

12.4.2 Estimation by Two Stage Least Squares (2SLS)

- We can estimate the above model by Two Stage Least Squares (2SLS)

- Step 1: First-stage regression(s)

- Run an OLS regression for each of the endogenous variables (\(X_{1i},\dots,X_{ki}\)) on all instrumental variables (\(Z_{1i},\dots,Z_{mi}\)), all exogenous variables (\(W_{1i},\dots,W_{ri}\)) and an intercept.

- Compute the fitted values (\(\widehat{X}_{1i},\dots,\widehat{X}_{ki}\)).

- Step 2: Second-stage regression

- Regress the dependent variable \(Y_i\) on the predicted values of all endogenous regressors (\(\widehat{X}_{1i},\dots,\widehat{X}_{ki}\)), all exogenous variables (\(W_{1i},\dots,W_{ri}\)) and an intercept using OLS.

- This gives \(\widehat{\beta}_{0}^{TSLS},\dots,\widehat{\beta}_{k+r}^{TSLS}\), the 2SLS estimates of the model coefficients.

12.4.2.1 Intuition

- Why does this work? Let’s go back to the simple example with 1 endogenous variable and 1 IV.

- In the first stage, we estimate

\[ x_i = \pi_0 + \pi_1 z_i + v_i \] by OLS and obtain the fitted value \(\widehat{x}_i = \widehat{\pi}_0 + \widehat{\pi}_1 z_i\). - In the second stage, we estimate \[ y_i = \beta_0 + \beta_1 \widehat{x}_i + u_i \]

- Since \(\widehat{x}_i\) depends only on \(z_i\), which is uncorrelated with \(u_i\), the second stage can estimate \(\beta_1\) without bias.

- Can you see the importance of both independence and relevance asssumption here? (More formal discussion later)

12.4.3 Conditions for Valid IVs in a general framework

12.4.3.1 Necessary condition

- Depending on the number of IVs, we have three cases

- Over-identification: \(M > K\)

- Just identification] \(M=K\)

- Under-identification \(M < K\)

- The necessary condition is \(M \geq K\).

- We should have more IVs than endogenous variables!!

12.4.3.2 Sufficient condition

- How about sufficiency?

- In a general framework, the sufficient condition for valid instruments is given as follows.

- Independence: \(Cov( Z_{mi}, \epsilon_i) = 0\) for all \(m\).

- Relevance: In the second stage regression, the variables \[ \left( \widehat{X}_{1i},\dots,\widehat{X}_{ki}, W_{1i},\dots,W_{ri}, 1 \right) \] are not perfectly multicollinear.

- What does the relevance condition mean?

- In the simple example above, The first stage is

\[ x_i = \pi_0 + \pi_1 z_i + v_i \] and the second stage is \[ y_i = \beta_0 + \beta_1 \widehat{x}_i + u_i \] - The second stage would have perfect multicollinarity if \(\pi_1 = 0\) (i.e., \(\widehat{x}_i = \pi_0\)).

- Back to the general case, the first stage for \(X_k\) can be written as \[ X_{ki} = \pi_0 + \pi_1 Z_{1i} + \cdots + \pi_M Z_{Mi} + \pi_{M+1} W_{1i} + \cdots + \pi_{M+R} W_{Ri} \] and one of \(\pi_1 , \cdots, \pi_M\) should be non-zero.

- Intuitively speaking, the instruments should be correlated with endogenous variables after controlling for exogenous variables

12.5 Check Instrument Validity

12.5.1 Relevance

- Instruments are weak if those instruments explain little variation in the endogenous variables.

- Weak instruments lead to

- imprecise estimates (higher standard errors)

- The asymptotic distribution would deviate from a normal distribution even if we have a large sample.

- Here is a rule of thumb to check the relevance conditions.

- Consider the case with one endogenous variable \(X_{1i}\).

- The first stage regression

\[ X_k = \pi_0 + \pi_1 Z_{1i} + \cdots + \pi_M Z_{Mi} + \pi_{M+1} W_{1i} + \cdots + \pi_{M+R} W_{Ri} \] - And test the null hypothesis \[

\begin{aligned}

H_0 & : \pi_1 = \cdots = \pi_M = 0 \\

H_1 & : otherwise

\end{aligned}

\]

- This is F test (test of joint hypothesis)

- If we can reject this, we can say no concern for weak instruments.

- A rule of thumbs is that the F statistic should be larger than 10.

12.5.1 Independence (Instrument exogeneity)

- Arguing for independence is hard and a key in empirical analysis.

- Justification of this assumption depends on a context, institutional features, etc…

- We will see this through examples in the next chapter.